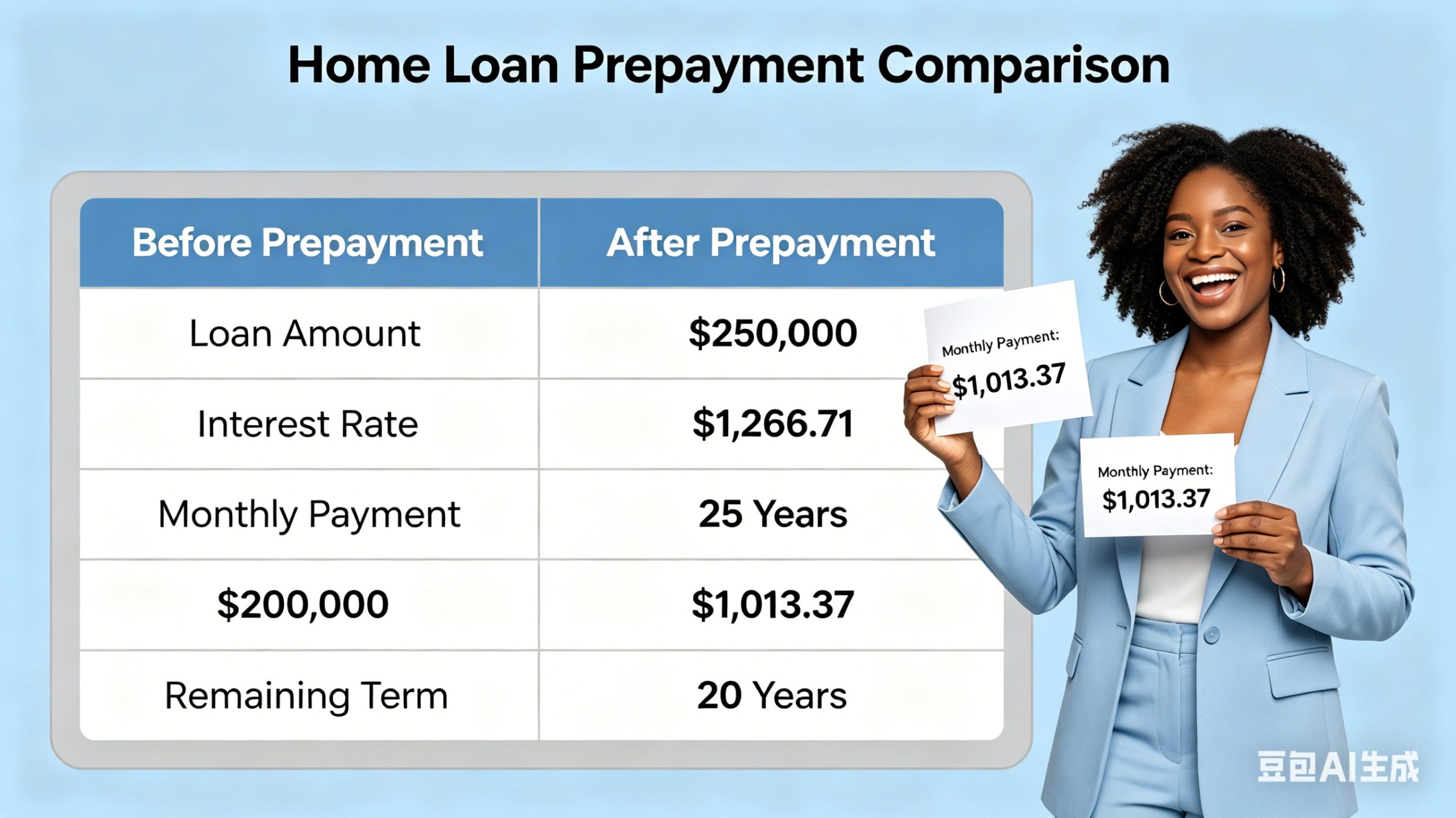

1. The “Pay Down Your Bond” Case: The Certainty of Interest Saved

Paying down a home loan is the most traditional “investment” in South Africa. Its logic is simple: every rand you prepay stops future interest from accruing, giving you a risk‑free, tax‑free return equal to your mortgage rate.

Baseline Assumptions

| Item | Value |

|---|---|

| Outstanding home loan | R2,000,000 |

| Remaining term | 15 years |

| Interest rate (prime lending rate) | 10.25% |

| Monthly instalment (principal + interest) | ~R21,100 |

| Total interest over 15 years | ~R1,800,000 |

After Prepaying R1,000,000

| Item | Value |

|---|---|

| Remaining principal | R1,000,000 |

| Total interest over 15 years (after prepayment) | ~R900,000 |

| Total interest saved | ~R900,000 |

Key advantages of prepaying

- ✅ Certainty – you know exactly how much you save.

- ✅ No market risk – no chance of losing capital.

- ✅ Immediate monthly cash flow improvement – your new instalment drops to ~R10,550, freeing up over R10,500 every month.

⚠️ But note: that R1,000,000 becomes locked in your home. If you need it later for an emergency, education, or a new opportunity, you would have to re‑borrow (at potentially higher rates) or sell the property.

2. The “Invest in Financial Markets” Case: Harnessing Compound Growth

Instead of prepaying, you could put the R1,000,000 into financial assets, using the 10.25% cost of debt as your “hurdle rate” – meaning your investments need to earn more than 10.25% pre‑tax to come out ahead.

Option A: Low‑Cost Global Equity ETF (e.g. S&P 500 or MSCI World)

Long‑term historical returns (pre‑inflation) are around 9‑10% per year. South Africans can buy these through local platforms like EasyEquities, Sygnia, or Satrix.

Assumed annual return: 8% (conservative)

| Period | Value |

|---|---|

| After 10 years | ~R2,158,000 |

| After 20 years | ~R4,661,000 |

Option B: JSE All‑Share Index Fund

The JSE has delivered long‑term average returns (including dividends) of about 7‑9% per year. No currency risk, but fully exposed to the South African economy.

Assumed annual return: 7.5%

| Period | Value |

|---|---|

| After 10 years | ~R2,061,000 |

| After 20 years | ~R4,247,000 |

Option C: High‑Yield Savings Account or Money Market Fund

Current high‑yield savings accounts in South Africa offer around 6‑7% per year (e.g. TymeBank, African Bank, Nedbank).

Assumed interest rate: 6.5% (before tax)

| Item | Calculation |

|---|---|

| Annual interest (gross) | R65,000 |

| Interest tax (on portion above R34,500, at e.g. 30% marginal rate) | ~R9,000 |

| After‑tax annual interest | ~R56,000 |

| 10‑year cumulative (not reinvested) | ~R560,000 |

Quick Comparison Table

| Strategy | Pros | Cons |

|---|---|---|

| Pay down bond | Risk‑free, tax‑free, improves cash flow | Capital locked, no upside potential |

| Global ETF | Long‑term growth, liquid, currency diversification | Short‑term volatility, currency risk |

| Local ETF | No currency risk, lower fees | Tied to SA economy, political risk |

| High‑yield savings | Principal safe, accessible | Low return, interest taxed |

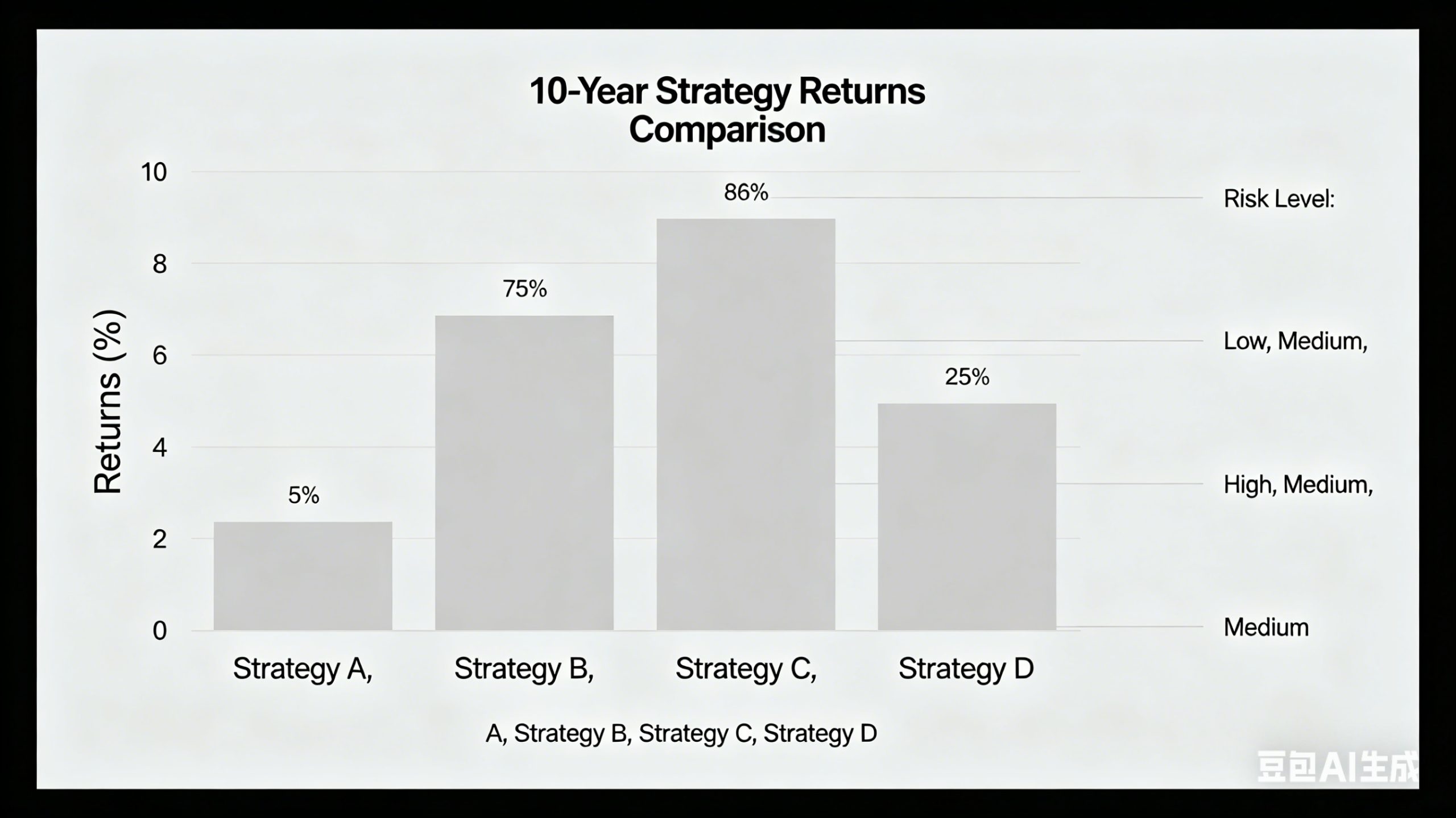

3. The 10‑Year Gap: What the Numbers Actually Look Like

Let’s project four strategies over 10 years, using conservative, realistic assumptions and including the cost of capital (the interest you would have saved by prepaying).

| Strategy | Estimated value after 10 years | Relative advantage vs. prepaying | Risk level |

|---|---|---|---|

| Pay down bond | ~R900,000 interest saved (indirect) | Baseline (R0) | None |

| JSE ETF (7% p.a.) | ~R1,967,000 | +R1,000,000 to +R1,500,000 | Medium |

| Global ETF (8% p.a.) | ~R2,158,000 | +R1,200,000 to +R1,800,000 | Medium‑high + currency |

| High‑yield savings (4% after tax) | ~R1,480,000 | Roughly break‑even or slightly negative | Very low |

📊 Historical note: Over any 10‑year period in the past 20 years, a globally diversified equity portfolio has outperformed mortgage prepayment more than 85% of the time. But past performance does not guarantee future results, and equities can experience sharp drawdowns (e.g. March 2020, 2022).

4. Six Real Factors That Should Drive Your Decision

Forget generic advice. Your personal situation determines which choice is better.

① Your mortgage interest rate

If your rate is above 12% (e.g. an older fixed rate loan), prepaying gives you a guaranteed 12%+ return – hard for any conservative investment to beat. If your rate is around 10%, the gap is narrower.

② Your risk tolerance

Imagine you invest R1,000,000 in the JSE, and next year the market drops 20% – your portfolio is now R800,000. Can you stay calm and hold? If not, prepaying or saving may be better.

③ Your cash flow situation

If your bond instalment already takes more than 35% of your after‑tax income, prepaying to lower that burden has significant “peace of mind” value. Financial comfort is a return in itself.

④ Your investment time horizon

- Short term (0‑5 years): avoid volatile assets. Prepay or use high‑yield savings.

- Long term (10+ years): compounding strongly favours equities.

⑤ South African tax environment

| Income type | How it’s taxed |

|---|---|

| Interest | First R34,500/year tax‑free; excess taxed at your marginal rate (18‑45%) |

| Capital gains (selling shares/ETFs) | 40% of gain added to taxable income; annual R40,000 exemption |

| Interest saved by prepaying | Fully tax‑free |

⑥ SARB interest rate outlook

Markets expect another 50bps cut later in 2026. Lower rates reduce your mortgage cost (good for keeping debt) and tend to boost equity markets (good for investing). But the window to lock in current yields may be closing.

5. Scenario Comparison: Four Typical Investor Profiles

| Profile | Recommended approach | Reasoning |

|---|---|---|

| Conservative, near retirement | Pay down bond (60‑80%) + high‑yield savings (20‑40%) | Capital preservation, reduced monthly outgo |

| Young professional, long horizon | Global ETF (70‑80%) + bond prepayment (20‑30%) | Capture compounding, keep some flexibility |

| Balanced, moderate risk | 50% ETF / 50% bond prepayment | Best of both worlds |

| Already low debt, high cash flow | Mostly equities (80‑100%) | Strong ability to weather volatility |

6. Popular South African Investment Platforms & Tools (Informational Only)

| Platform | Focus | Suitable for | Fee level |

|---|---|---|---|

| EasyEquities | Fractional shares, US/SA stocks | Beginners, small monthly amounts | Low |

| Satrix | JSE‑listed ETFs | Passive local index investors | Low |

| Sygnia | Multi‑asset ETFs, offshore funds | Long‑term allocators | Low‑medium |

| TymeBank / African Bank | High‑yield savings | Emergency funds, conservative savers | No fees |

This is for information only and does not constitute advice. Always do your own research or consult a licensed financial advisor.

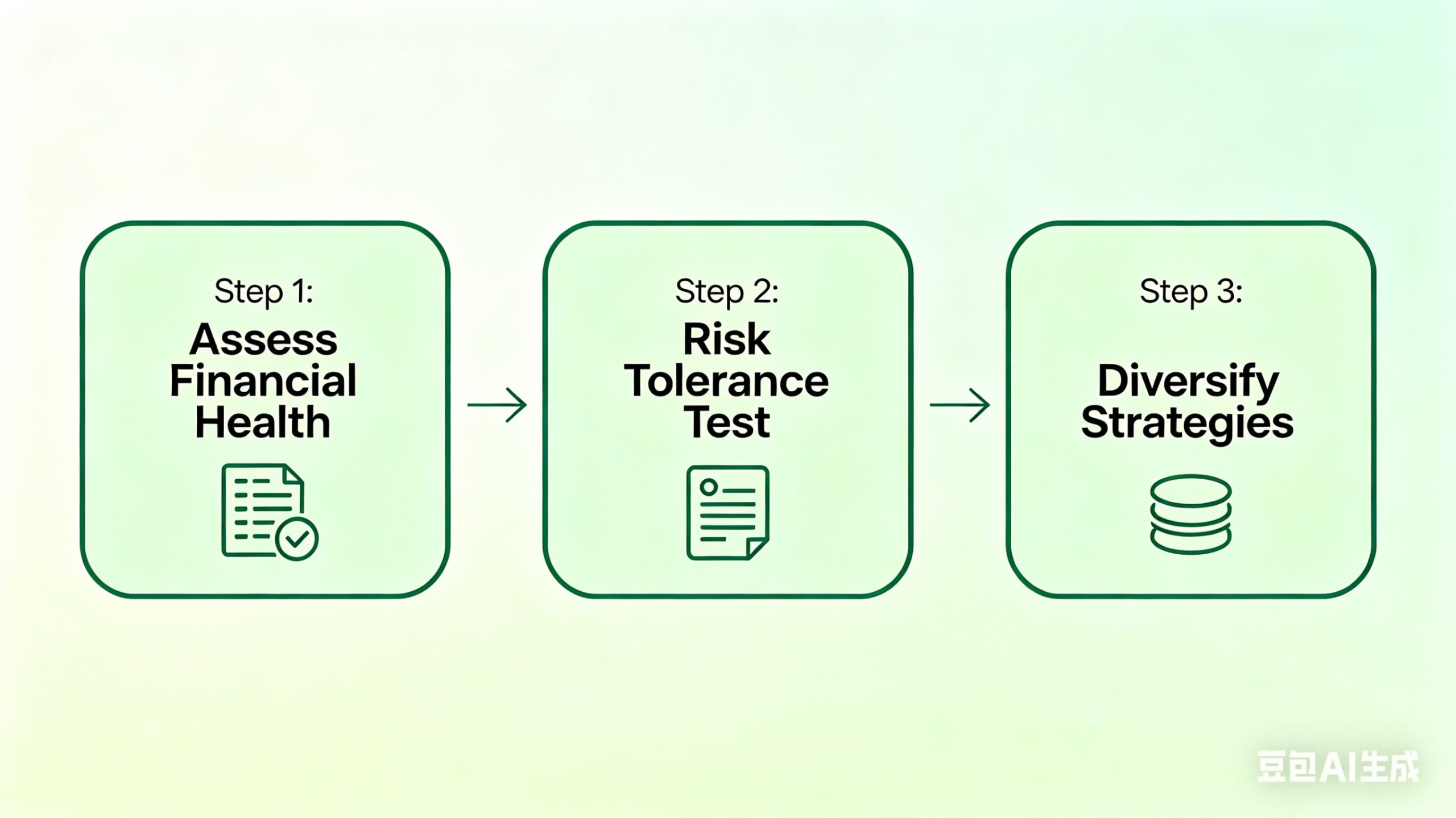

7. Three Steps to Your Own Optimal Decision

Step 1 – Assess your financial health

- Do you have a 6‑12 month emergency fund? (R100,000 – R200,000)

- Is your bond instalment >35% of after‑tax income?

- Do you have any higher‑cost debt (credit cards, personal loans at 15‑25%)? Pay those first.

Step 2 – Take a simple risk tolerance test

Ask yourself: if R1,000,000 in equities dropped to R800,000 in one year, would you feel anxious enough to sell? If yes, you are more conservative than you think – lean toward prepaying.

Step 3 – Diversify across strategies

You don’t have to go all‑in on one option. A typical split example:

- 💰 R300,000 – prepay your bond (certainty, lower monthly payments)

- 📈 R400,000 – global equity ETF (growth potential)

- 🏦 R300,000 – high‑yield savings (liquidity, safety net)

This way you benefit from compounding, while keeping a safety cushion and reducing debt.

8. Final Takeaway: Personal Finance is Personal

Paying down debt and investing are not enemies. They are different tools in your financial toolbox.

- Choose prepaying if your priority is reducing fixed monthly costs, lowering risk, and you value certainty over higher possible returns.

- Choose investing if you have a long time horizon, can tolerate short‑term market drops, and want to harness the power of compound growth.

The South African rand slowly loses purchasing power over time. Historically, productive assets like equities have been the only reliable way to stay ahead of inflation – but no asset class goes up every year. The right decision is the one that lets you sleep well at night while still moving you toward your financial goals.